Can financial inclusion help india achieve sdgs in covid era?

Play all audios:

LIKE ANY OTHER CRISIS, COVID-19 PRESENTS A UNIQUE OPPORTUNITY FOR POLICYMAKERS AND OTHER STAKEHOLDERS TO WORK TOWARDS REALISING THE DREAM OF CREATING A TRULY DIGITAL ECONOMY WHICH WOULD HELP

BRIDGE DIGITAL DIVIDE BETWEEN URBAN AND RURAL AREAS. FINANCIAL INCLUSION WOULD EMERGE AS THE STRONGEST PILLAR PIGGYBACKING ON AGENT NETWORK. DELIVERY OF FINANCIAL SERVICES CAN POTENTIALLY

BECOME MORE STRUCTURED AND ORGANISED. IN THE BEGINNING OF 21ST CENTURY, WITH MANY COUNTRIES OF THE WORLD GRAPPLING WITH SOCIAL AND ECONOMIC PROBLEMS SUCH AS POVERTY, HUNGER, INEQUITY AND

TERMINAL DISEASES, UNITED NATIONS THOUGHT OF ENTRUSTING A GROUP OF FEW NATIONS WITH THE TASK OF ERADICATING SUCH ISSUES FROM THE WORLD. THESE NATIONS WERE SUPPOSED TO MAKE CONCERTED EFFORTS

AGAINST FEW MEASURABLE TARGETS AND ADDRESS SUCH CHALLENGES IN A STRUCTURED MANNER. THUS, IN THE YEAR 2001, MILLENNIUM DEVELOPMENT GOALS (MDGS) WERE INTRODUCED WITH A SET OF 8 MILLENNIUM

GOALS STARTING FROM ERADICATION OF POVERTY TILL HALT OF TERMINAL DISEASES LIKE AIDS ETC. WITHIN NEXT 15 YEARS TILL 2015. HOWEVER, SOON UN REALISED THAT PROGRESS SO MADE CONSIDERING THE MDGS

WAS NOT DEPICTING THE REAL PROGRESS DUE TO NARROW TARGET/INDICATORS FRAMEWORK OF MDGS. THUS, IN 2015, SUSTAINABLE DEVELOPMENT GOALS (SDGS) SUCCEEDED MDGS AND WERE ADOPTED BY UN AND ITS

MEMBER STATES PROCLAIMING BETTER INDICATORS AND TARGET FRAMEWORK EXTENDING 8 MDGS TO 17 GLOBAL GOALS TO BE ACHIEVED BY 2030. THESE GOALS EXTEND FROM ERADICATING POVERTY TO INCLUDE

SUSTAINABLE CLIMATE ACTION AND FOSTERING GLOBAL PARTNERSHIPS FOR SUSTAINABLE DEVELOPMENT. HOW THESE SDGS MAKE SENSE FOR COUNTRIES LIKE INDIA? For many developing countries like India with a

large population struggling with social, economic and environmental challenges, SDG framework helps to prepare agenda and policies by Government against some quantifiable and measurable

targets to address such challenges which can foster sustained and inclusive growth. It brings sustainable development as a collective exercise involving the ministries of country from

central to state levels assuming collective responsibility for progress and impediments. Even before the 17 SDGs were shaped, India was committed to bringing social and economic balance in

the society, the reason why its national goals get reflected in the SDGs, so adopted. National Institution for Transforming India (NITI) Aayog, India’s think tank, chaired by PM of India,

has been entrusted with the task of leadership and coordination for the SDG progress in India. The institution has carried out a detailed mapping of the 17 Goals and 169 targets to Nodal

Central Ministries, Centrally Sponsored Schemes and major government initiatives. Similar mapping has been carried out by many state governments setting targets for respective states. NITI

Aayog publishes SDG India Index created in collaboration with the Ministry of Statistics and Programme Implementation (MoSPI) and United Nations in India. This index depicts progress made by

various states and UTs in India against the SDG targets. FINANCIAL INCLUSION AND SDGS United Nations recognises Financial inclusion (FI) as an enabler and facilitator of SDGs as it can

support overall economic growth. Financial Inclusion has enormous potential in leaving positive impact on at least 8 out of the 17 SDGs namely, _SDG1 ON ERADICATING POVERTY; SDG 2 ON ENDING

HUNGER, ACHIEVING FOOD SECURITY AND PROMOTING SUSTAINABLE AGRICULTURE; SDG 3 ON PROFITING HEALTH AND WELL-BEING; SDG 5 ON ACHIEVING GENDER EQUALITY AND ECONOMIC EMPOWERMENT OF WOMEN; SDG 8

ON PROMOTING ECONOMIC GROWTH AND JOBS; SDG 9 ON SUPPORTING INDUSTRY, INNOVATION, AND INFRASTRUCTURE; AND SDG 10 ON REDUCING INEQUALITY AS WELL AS SDG 17 ON PARTNERSHIP FOR GLOBAL GOALS._

Financial Inclusion defines itself as financial services — such as deposit and savings accounts, payment services, loans, and insurance — readily available to consumers who are actively and

effectively using these services to meet their specific needs (GPFI 2011). We understand that access to financial services has multi-fold effect on the progress of SDGs. Improved access to

financial services leads to improvement in economic growth indicators which further strengthens the framework for inclusive finance thus, supporting in further enhancement and

diversification of financial service portfolio as available to the last mile beneficiary. The journey of FI in India has been eventful, to say the least. It has had its fair share of

successes and failures. The progress has been gradual with many a spike sprayed in between. Though FI as a concept, in some form or the other, has been in place for decades now, the more

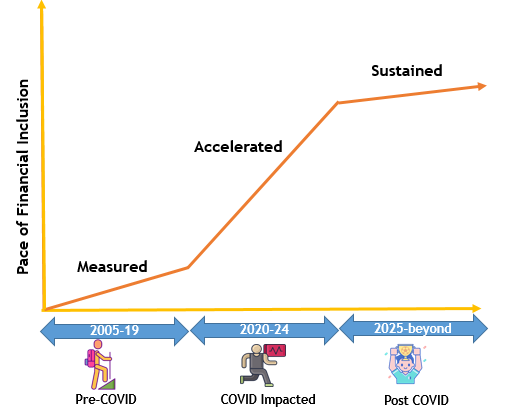

concerted push can be traced back to the 2005 when the agency-led banking structure was first proposed as a state policy to accelerate the efforts towards banking the un-banked. Since then a

lot of water has flowed under the bridge. India has now become close to universally banked, though not very active in transacting through those bank accounts. Digitisation of the banking

and payment systems has leapfrogged to a state where they have become important tools for framing policies not just for the blue-blooded stratum but also for the poor and the marginalised.

FI has led to empowerment of women-folks, thus bridging the gender divide to an extent. This and some of the other key initiatives undertaken under the FI umbrella are captured in the figure

below, especially in relation to their impact on key SDGs. ROLE OF FI IN DRIVING SDGS DURING AND AFTER COVID ERA While, FI fast paced India’s journey towards achievement of SDGs from

2005–2019, outbreak of COVID-19 has certainly put a question mark on the progress ahead. The pandemic which has till date affected 4.8 million population worldwide and 0.1 million in India

alone, has slowed down the economic activities and banking operations for an indefinite period. This calls for action by all stakeholders in the economy to come forward and plan for

concerted initiatives in order not to impact the progress of greater financial inclusion. Like any other crisis, COVID-19 presents a unique opportunity for policymakers and other

stakeholders to work towards realizing the dream of creating a truly digital economy which would help bridge digital divide between urban and rural areas. Financial Inclusion would emerge as

the strongest pillar piggybacking on agent network. Delivery of financial services can potentially become more structured and organized. The crisis necessitates the state to ensure that

principles of social distancing are practiced in both letter and spirit for an extended time which may stretch upto next 3–4 years till the time the last Indian is vaccinated against COVID.

This requires business to go contact-less and online even in hinterland which includes financial services as well. This essentially would manifest itself into pumping in more money towards

strengthening digital infrastructure in the Hinterland, viz. low cost POS terminals, reduced MDR for merchants facilitating transactions, truly broadband connectivity upto the last mile,

e-commerce platforms focusing rural and TIER-III cities and towns, and finally, the concept of doorstep delivery of goods, services including financial services. While thinking aloud on the

opportunity this crisis creates for each section of financial services industry, following initiatives in Financial Inclusion space may come to the fore during and Post-COVID: Return on

investment in above initiatives are bound to be rich and sustainable which would be seen in Post-COVID phase after 2024 and beyond. The FI initiatives taken during COVID time would

potentially empower the villages of India. An empowered village would have more time and money to spend productive time on entrepreneurial activities creating employment in the villages. A

strong village economy will strengthen the overall health of Indian economy while having ripple effect on better education, low migration to urban areas, higher employment, reduced hunger,

poverty alleviation, essentially a smooth sail towards achievement of SDGs for India. CONCLUSION Considering the above assessment of Financial Inclusion as a tool and an enabler, it is fair

to assume its importance to policy makers in leading the country out of this grave existential threat of our era i.e. COVID-19. It always had enormous potential in driving all-round growth

of not just the Indian economy, but overall development of an inclusive Indian society. This scope and potential of FI has only accentuated in these times of this pandemic which has, as any

other natural or man-made calamity, affected the people on fringes the most. And as is evident from above relation between FI and many of the SDGs, an honest effort towards expanding and

strengthening FI in this country is bound to enormously improve many of our SDG indicators and help create a better, equitable, healthier and sustainable society for all of us to live in.